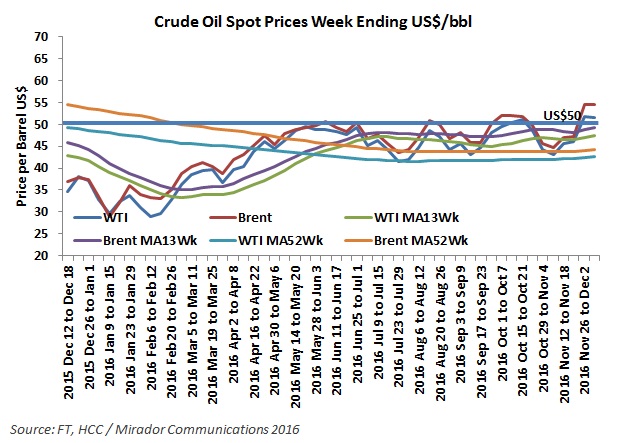

The OPEC announcement in Vienna a few weeks ago pushed oil prices up, pushed stock markets up in oil exporting countries and got everyone thinking that the worst was finally over.

The tax reform is poised to be the dominant issue in this month as 2016, and the congressional session, winds to a halt. The oil industry has submitted its wish list, but the financial shortfalls of the government’s budget makes any landmark gains look unlikely.

Ecopetrol (NYSE:EC) 3Q16 Line of Business (LoB) results show that Refining is once again profitability challenged while E&P is getting better all the time.

Donald Trump’s eminent possession of the White House has the Mexican peso in a tailspin: it is down over 10% since election day. The President-elect is an external factor.

With all quarterly-reporting public companies now in our database, we can update our trend graphs for netback and average realized oil prices.

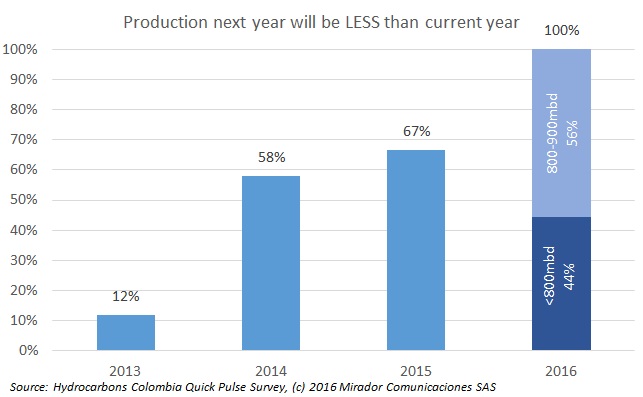

We have been tracking some questions for several editions of our Quick Pulse survey and that allows us to look at how pessimism has changed over the recent past; the evolution of ‘bad’ if you will.

Government negotiators and Farc spokespersons announced that a new peace agreement had been achieved. However, I wonder if this really means that we are closer to the post-conflict in Colombia or whether this is still way off in the distance.

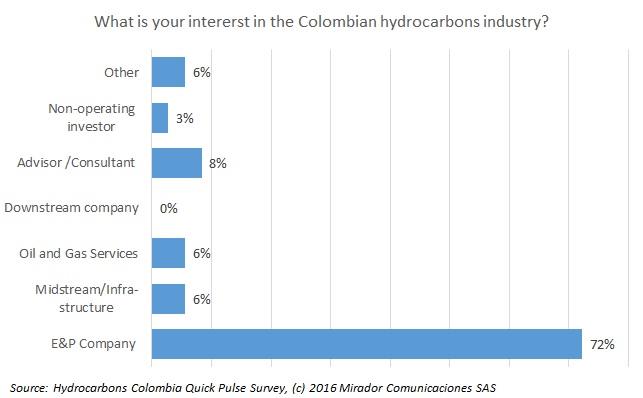

This week we temporarily merge our ‘From our analyst’s desk’ and ‘What we think’ features to analyze what you think.

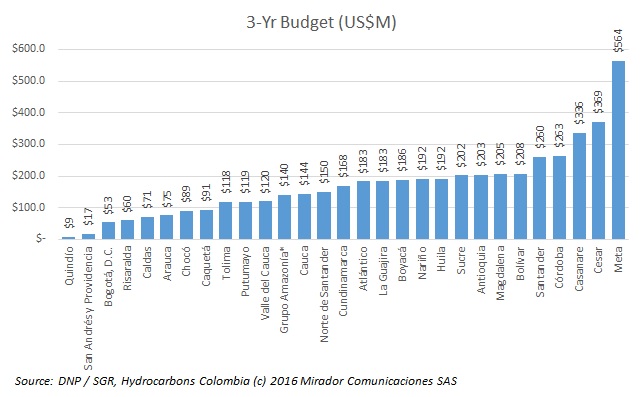

Caquetá represents the new frontier for oil production in Colombia, a region with promising potential to develop reserves and a basin without much activity thus far, especially if the armed conflict ceases.

This week we published a press release by the senator from Meta, Maritza Martínez where she accused the recently-approved royalties budget of being unfair to Llanos producers including her home department.

2026, Hydrocarbons Colombia, All Rights Reserved.