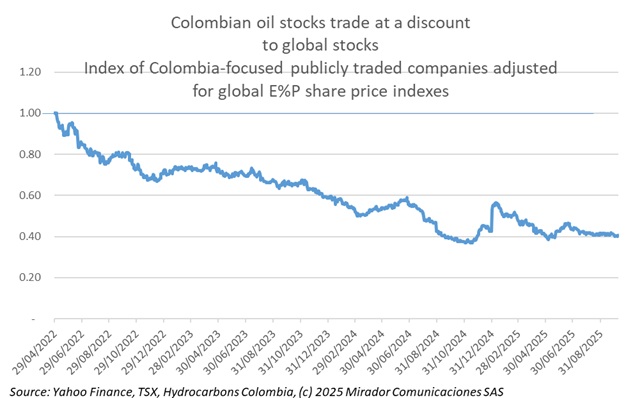

We have updated our index of the stock prices of Colombian-focused, publicly listed companies to the latest data and rebased so that the index begins on May 1 2022, perhaps the last time that anyone might have hoped that Gustavo Petro would not become president of Colombia. This makes comparisons easier and leaves no doubt that Colombian E&Ps, including Ecopetrol, have suffered from his administration.

Earlier this month the Colombian-Canadian Chamber of Commerce held its annual Dialogo Canada day, an event that discusses Colombian policy topics of interest to the major Canadian investment groups in the country. The session on hydrocarbons featured a discussion between Orlando Velandia, president of the industry regulator, the ANH, and two industry representatives, Gran Tierra’s Country Manager, Diego Perez-Claramunt and Parex’s Government Affairs VP, Rafael Pinto.

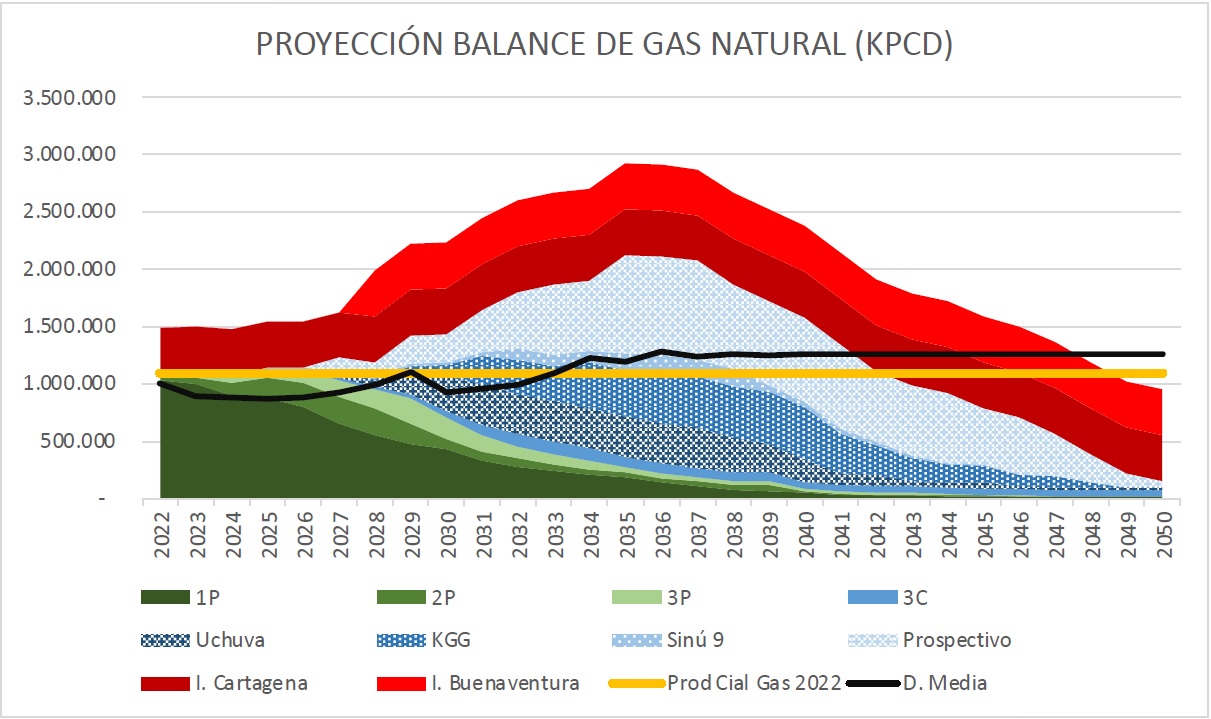

In January of 2023, I wrote an article entitled Don’t get me wrong critiquing a report by the Ministry of Energy proving that Colombia had lots of gas, enough to export in fact. How did that work out?

Oil and gas industry companies in Colombia with foreign investors have no doubt had to answer questions this week about the US government’s decision to “decertify” the country. What does this mean and what do we think of the impact?

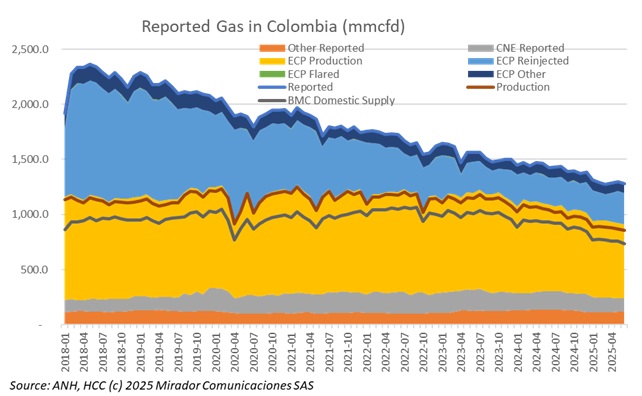

Everyone in the industry worries about natural gas production falling because that means more imports and higher prices for gas users and for electricity users. So why does it continue to decline?

There is a lot happening in the industry and whenever members get together there is lots to discuss. What do they talk about?

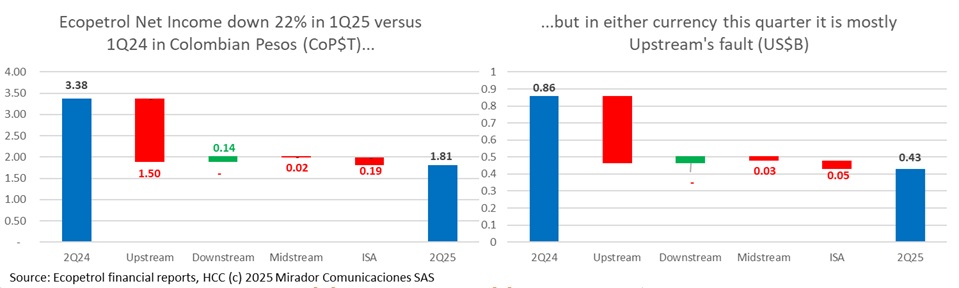

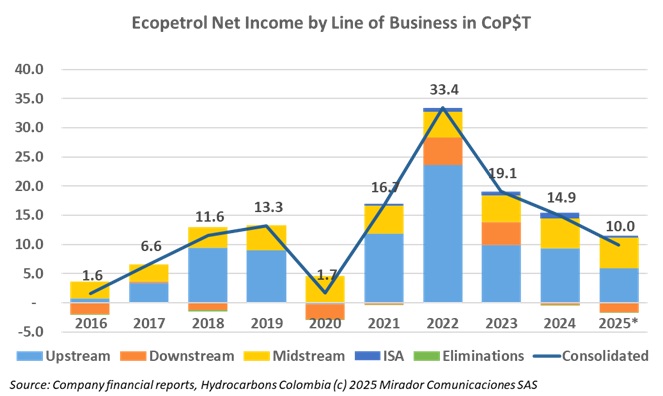

Ecopetrol’s deteriorating Net Income continues to consume (virtual) column inches in the Colombian business press. Our perhaps counter-to-the-current view has been that short-term financial performance is the wrong place to look for what might be wrong with the NOC. This week we dive deeper into the qualitative comments we made last time.

…but we think about them anyway.

… but who’s fault is it?

The Colombian press certainly wants to blame the current administration – either the company’s or the country’s – for the NOC’s declining financial performance. Management blames oil prices which are, most certainly, down over last year. Our previous analyses have supported management’s thesis about short-term, tactical performance, even as we seriously question mid and long-term strategy. Now we have another bad quarter.

We called last week’s opinion article in ePower Colombia “One year more” on the last year of Gustavo Petro’s mandate. Apparently only one person opened the article, and that might have been our editor, preparing for this week’s HCC opinion. Maybe we are all just tired of thinking about Colombian politics and the current government.

2026, Hydrocarbons Colombia, All Rights Reserved.