The Energy Institute took over production of the annual Statistical Review of World Energy which BP had produced for decades. This was, in fact, the 75th edition. We find it interesting for the tables and tables of energy data cut every which way that can produce thought-provoking graphs.

Tomás de la Calle is back, this time looking at the country’s declining gas reserves and wondering about the UPME’s role in getting us to here … and getting us back to self-sufficiency.

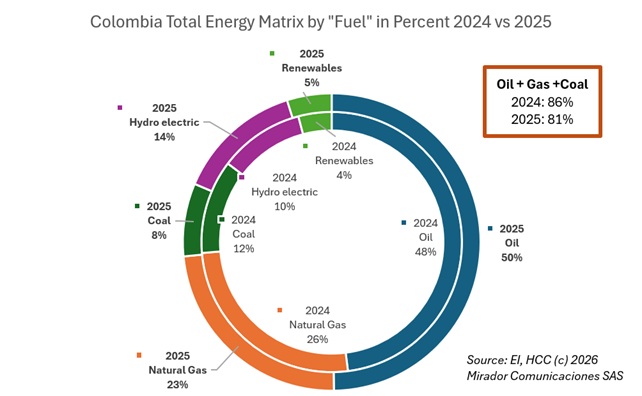

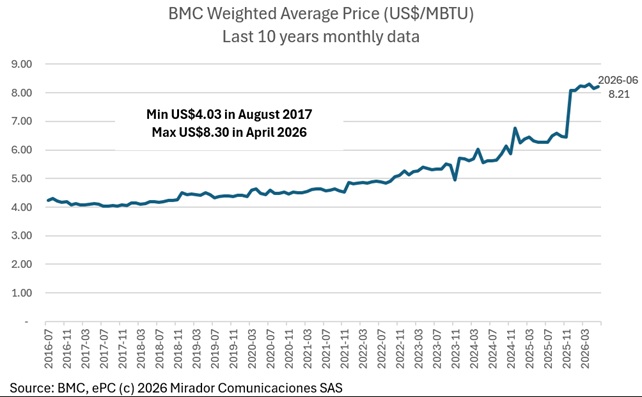

The El Niño weather phenomenon means less water behind hydro dams, less hydroelectricity produced and more need for gas-powered thermoelectricity. That plus the need to import LNG means gas prices should be going up.

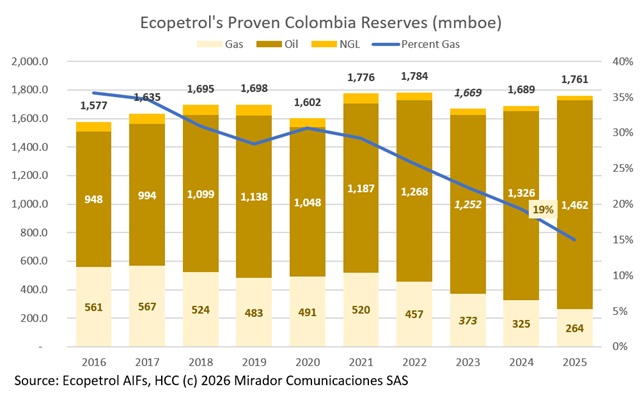

The National Hydrocarbons Agency (ANH) finally released Colombia’s total oil and gas reserves figures for year-end 2025 last week. Contributor Tomás de la Calle looked at Colombia’s oil reserves over the past nine years and even looked back thirty years to assess performance.

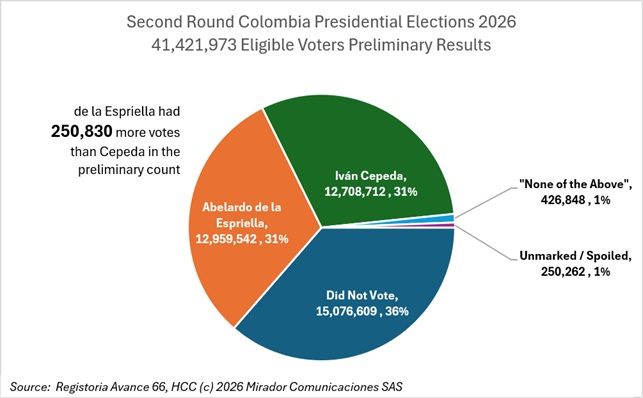

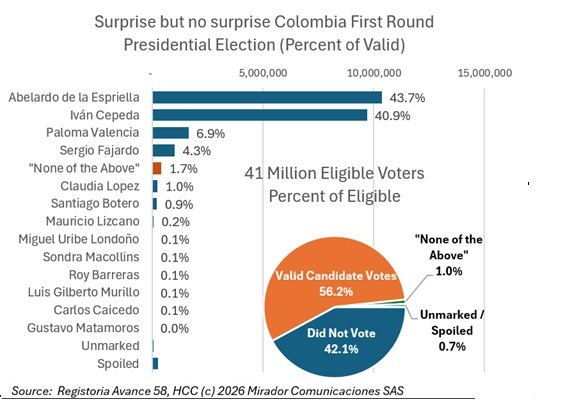

Yesterday’s presidential voting had a declared winner but the results are not definitive and the loser is contesting the result.

Or the dominance of Ecopetrol in Colombian statistics means what it does pulls the national conclusions. In any event, 2025 was another weak year for exploration and discoveries. Sharp pencils and improved recovery saved ECP’s reserves from falling.

The Iran War brought a welcome boost to oil prices that will benefit E&Ps throughout this year and into next. But will it also spur an end to the Internal Combustion Engine which has dominated transportation (and other applications) for over a century?

The expected candidates made it through to the second round and official government candidate Iván Cepeda got the approximately 40% of the vote that the polls said he would. But Abelard de la Espriella surprised by getting over 43% and coming first.

So earnings season comes to an end and, apart from a few special charges, a generally positive one. Brent over US$100/bl will do that. But, unsurprisingly perhaps, that is not what people are talking about

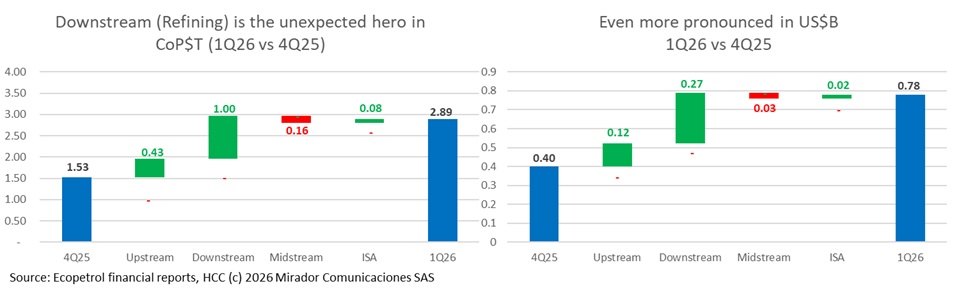

This week Ecopetrol published its financial results for the first quarter and the company received the usual criticism. We wrote briefly about our opinion – higher Brent means better results – and this long article will get deeper “under the hood”.

2026, Hydrocarbons Colombia, All Rights Reserved.