Aval Asset Management raised its price target for Ecopetrol shares to CoP$2,950, a 27% increase over its prior valuation, though the firm maintains a neutral rating given ongoing operational and financial challenges.

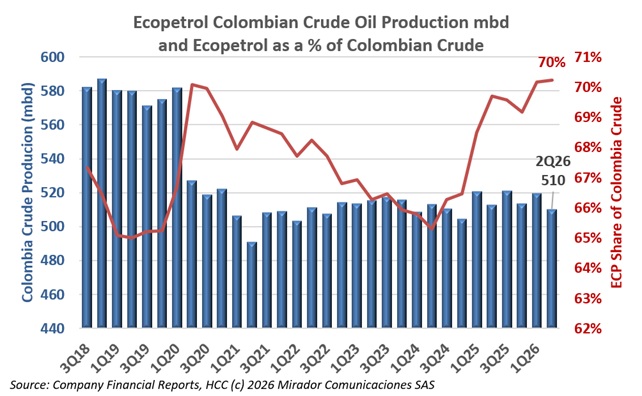

An El Heraldo feature gathering multiple sector experts makes the case that Ecopetrol’s decline under the outgoing government reflects deliberate policy choices, not just market conditions: 13 consecutive quarters of falling profits, crude production down 2.7% to 725,200 bd, and a leadership scandal involving outgoing president Ricardo Roa.

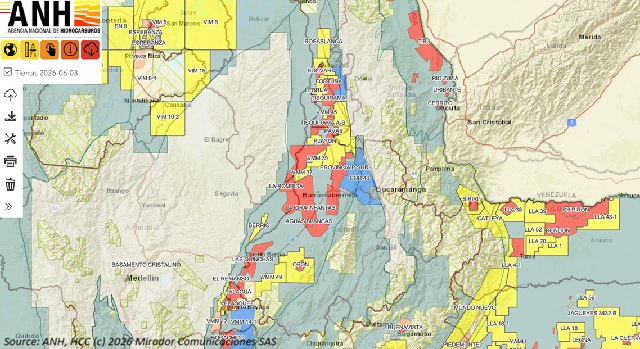

The collaboration agreement between Ecopetrol and Parex Resources for joint development of the Casabe, Casabe Sur, Peñas Blancas, and Llanito fields in the Magdalena Medio took effect July 30th, after satisfying all suspensive conditions including approval from the Superintendencia de Industria y Comercio (SIC).

Petrobras and Ecopetrol confirmed a new natural gas discovery with the drilling of the Sandía-1 exploration well, located in the GUA-OFF-0 block in deep water offshore Colombia.

Grupo Ecopetrol reported second-quarter 2026 results reflecting what the company described as its ability to maximize an integrated strategy and respond with agility to market dynamics.

Ecopetrol has taken action to have illegally copied information from roughly 15 companies within its business group removed from public access, working in coordination with the Fiscalía General de la Nación and the Ministry of Information and Communications Technology (MinTIC),

Back for only a single day, Ricardo Roa delivered his farewell address as Ecopetrol president on July 30th, closing a tenure marked by controversy that now has him facing judicial scrutiny.

Ecopetrol raised its natural gas contribution to 97 GBTUd to help cover the deficit created by the scheduled maintenance of the SPEC LNG regasification plant, which ran from Thursday, July 30th to Monday, August 3rd.

Vice president-elect José Manuel Restrepo delivered the incoming government’s clearest statement yet on Ecopetrol’s future, declaring that the new administration will pursue “a thorough transformation starting with the structural, strategic issue” at the state oil company.

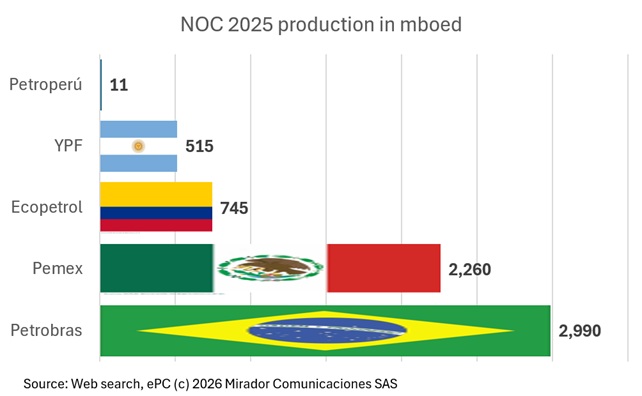

Higher oil prices and solid operational performance will not automatically translate into stronger credit quality for Latin America’s state-owned oil companies, according to a Moody’s report.

2026, Hydrocarbons Colombia, All Rights Reserved.