Sustained oil and gas growth since the early 2000s and plenty of potential for further E&P, although to achieve it operators will have to go offshore or operate amongst the complexities of the Amazon.

Recently, the State Council issued a confusing ruling on the deductibility of royalty payments, especially those paid with respect to concession contracts for the extractive sector.

Last week, we published about a court ruling that (supposedly) would lead to taxing royalties (technically, removing a ‘deduction’ for royalties).

Hard to believe but this is our fifth anniversary. Our website came up in late October of 2012 and our first daily newsletter dates from that time as well.

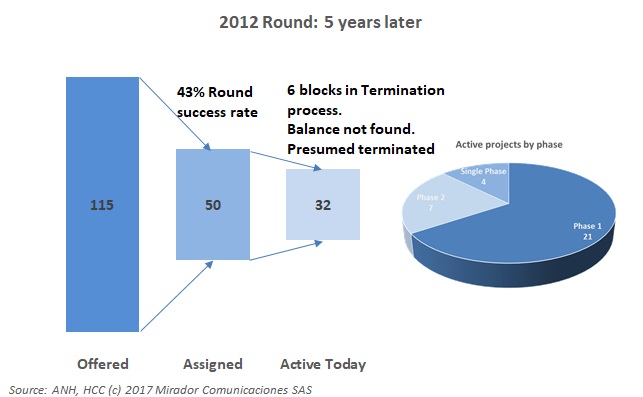

As noted in today’s companion article, the first major even that we covered was the 2012 Round of block auctions in the month of October.

When we were first starting out in HCC, I was fascinated by the paradox of successful ‘small’ companies in the Colombian industry and yet the government’s apparent desire to limit their scope in favor of ‘large’ companies who, frankly, seemed largely uninterested.

At one point in time we reported this weekly. Now quarterly seems it might be too frequent. The numbers are way down but do not seem to be telling the whole story.

A reader asked me why we had said that the research on unconventional had already been done. I told him it was because there was a time in 2013 and 2014 when it appeared as if fracking was just around the corner.

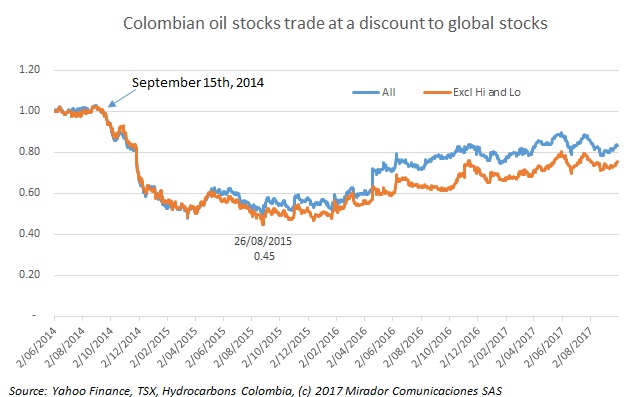

Every quarter we track the so-called ‘Colombian discount’ – the apparent penalty that the stocks of Colombia-focused producers bear relative to their global peers.

The Colombian-Canadian Chamber of Commerce (CCCC) hosted the third “Entrepreneurial Challenges for Peacebuilding in Colombia” forum, where industry representatives and state officials gave their opinion on how the industry can contribute to the post-conflict process taking place in Colombia.

2026, Hydrocarbons Colombia, All Rights Reserved.