So earnings season comes to an end and, apart from a few special charges, a generally positive one. Brent over US$100/bl will do that. But, unsurprisingly perhaps, that is not what people are talking about

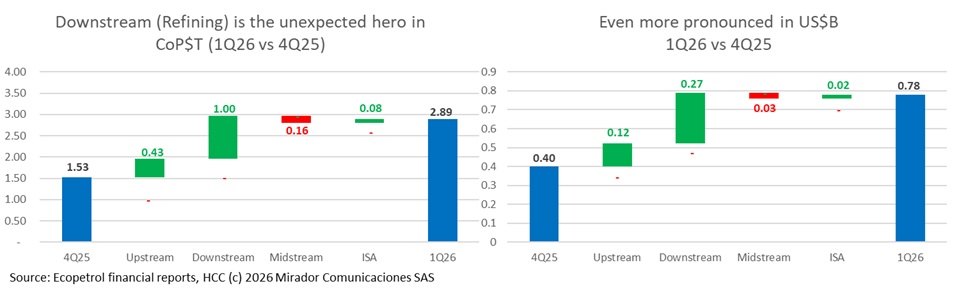

This week Ecopetrol published its financial results for the first quarter and the company received the usual criticism. We wrote briefly about our opinion – higher Brent means better results – and this long article will get deeper “under the hood”.

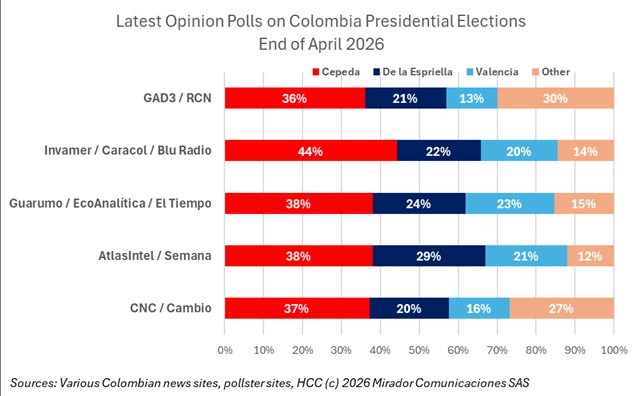

I had dinner this week with some industry members and, unsurprisingly, the election and what comes next – the topic of last week’s long article – was top of mind.

With the poll results from the end of April and with less than a month to the first round of the presidential elections in Colombia, it looks increasingly probable that Iván Cepeda, the candidate of the current administration’s political movement, will be the next president of Colombia.

Last night, while watching the news on TV, my wife asked me if I supported fracking. Given that her interests are in other fields, I knew the debate has become mainstream.

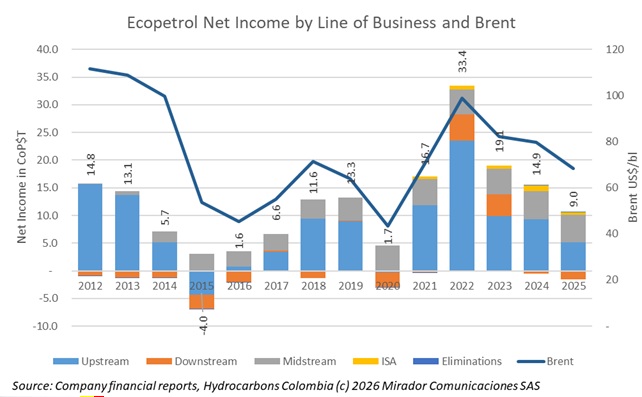

In a televised council of ministers in February, Colombian President Gustavo Petro said Ecopetrol would be bankrupt if oil fell below US$60/bl. We don’t expect Petro to get his sums right but we thought we’d better check, just in case.

A couple of weeks ago we reported President Gustavo Petro’s declaration that Colombia would withdraw from the international investment arbitration system, leaving only local courts to settle contract disputes. We wanted to go a bit deeper into this.

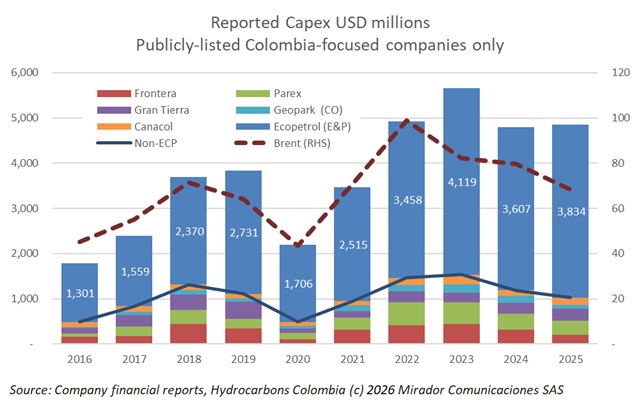

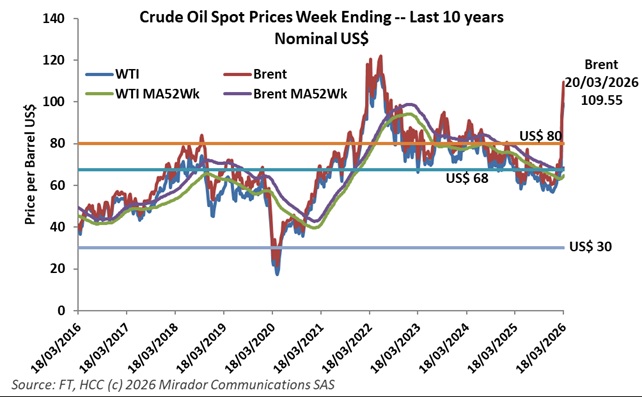

Our 2026 publishing plan called for a discussion of CAPEX and Brent assumptions this week since we expected to have the major companies’ 2025 reports. We will do that but the Iran War has played havoc with oil prices and President Donald Trump’s speech the other night apparently reassured no one that global crude markets would return to normal anytime soon.

No one can say 2026 has been uneventful in the oil and gas sector. A bidding war for Frontera’s E&P assets, potential for a change in the economic program in Colombia with a new president on August 7th and the Iran War send Brent up over US120 are but a few of the noteworthy items. Perhaps the biggest for Latin America with important implications for Colombia is the US intervention in Venezuela which promises to revitalize that country’s oil and gas production. However, will the promise be realized and what are the opportunities for companies in Colombia? We asked Jorge Neher, a Venezuelan Partner at Dentons Cardenas and Cardenas, who has lived and worked in Colombia for almost two decades, with deep knowledge of both countries’ oil and gas sectors, to tell us what is happening on the ground and how things could play out.

Some readers may think we are ignoring the sector’s most important news: the Iran War and its impact on oil prices. Instead, we worry about reporting things you already know, especially those that are widely reported global stories. Here we update our price charts for those who use them and try to make relevant Colombia-specific comments on what are rapidly changing events.

2026, Hydrocarbons Colombia, All Rights Reserved.