A week from when this is published, there will be a new administration running the energy sector in Colombia. If they have not already done so, members of the current team will be packing up their personal effects (beloved coffee mugs, family photos) and polishing their resumes to work on what comes next in their careers (but will not get them in trouble with Colombia’s conflict-of-interest regulations). How did they do in the job that is coming to an end?

Last Wednesday, July 20th 2022, the new Colombian Congress was sworn in. Despite the arithmetic we did at the time it was elected (way back in March) and again when the presidential elections concluded (just over a month ago), the majority is now supporting Gustavo Petro. Who would have thought it? I certainly did not but I should have.

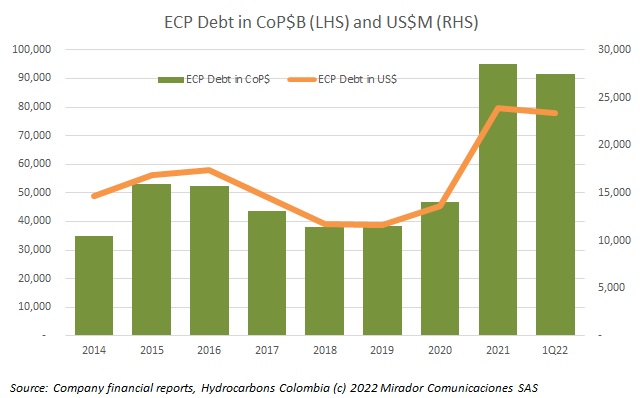

The story was titled basically “Everyone in the world is reducing their debt – except Ecopetrol”. Well, we have all had problems with our credit cards from time to time. Unable to resist that bright shiny thing – like ISA, for example – when we are already had unexpected expenses, like Covid-19 for example.

President-elect Gustavo Petro’s ministerial candidates are talking to the press and his energy strategy is becoming clearer. We do not know everything but we know more than we did before the election.

No one likes to be blamed for something they didn’t do. In the days following Gustavo Petro’s victory in Colombia’s recent presidential elections, Colombia-focused oil and gas stocks nosedived, with Ecopetrol in particular losing over 25% of its value at one point. Petro says “I’m not to blame” saying all oil and gas stocks were in decline because of the inevitability of energy transition. Let us use the data to see if he is right.

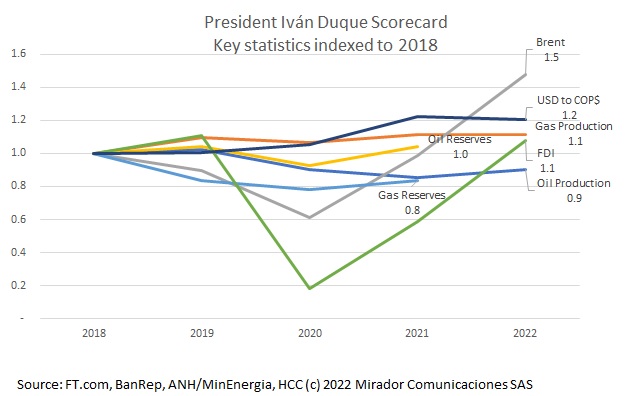

I was at a conference this week (not virtual!) and, inevitably, all the meals were served buffet-style (which we used to call smorgasbord – but have not seen that word much lately). Inspired by this, my commentary will be a little bit of one thing and some of another: Petro, oil prices, President Duque’s legacy and whatever else inspires – or maybe less. Inevitably as well at a buffet, one’s ambitions exceed one’s capacity.

Colombia was a charter member of the Washington Consensus and although some “true believers” of former-president Álvaro Uribe might disagree with me, the country has followed the liberal economic order for more than 25 years, certainly as long as I have been here. Now that consensus is almost certain to change.

Juan Pablo Ruiz is my favorite Colombian environmentalist because he is completely rational, completely pragmatic without losing one bit of his passion and commitment. Recently, he wrote a pair of columns directed at Colombia’s future president that touched on the strategy of reducing demand or supply of fossil fuels. I might have written them or at least something like them.

It is only the first quarter so our simple projections are highly suspect, and we will concentrate on relative measures. Conclusion: higher prices are a good thing even for Ecopetrol’s feeble Refining Line-of-Business (LoB). There. You don’t have to read the article. Except to look at the graphs.

Here we are again. A Manichean contest between left and right with both sides casting the other in the role of Satan. On Sunday, May 29th, Gustavo Petro and Rodolfo Hernández won the right to a runoff on June 19th to see who will be the president of Colombia.

2026, Hydrocarbons Colombia, All Rights Reserved.