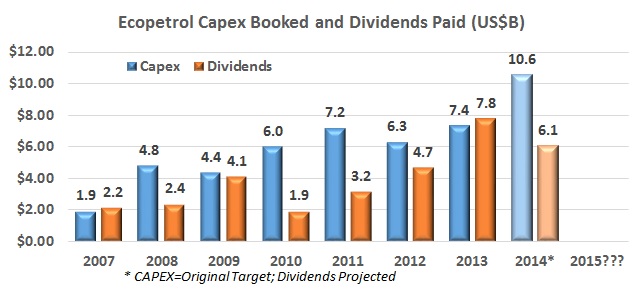

Ecopetrol (NYSE:EC) is planning to detail its investment plan for 2015, and, with a falling oil price, its Capex budget will have to drop, as speculation swirls around what other measures the NOC might have to take because of the new price scenario.

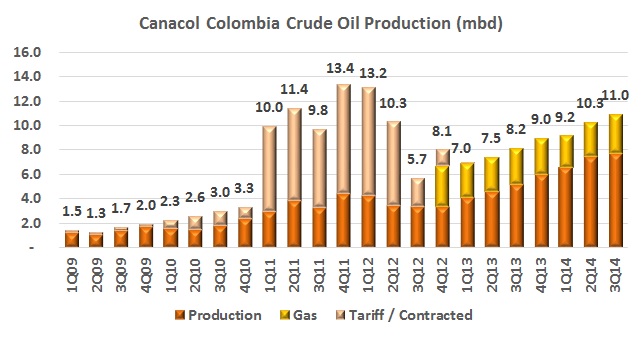

Canacol Energy (TSX:CNE) reported an increase in production and revenue growth for its first quarter of the 2015 fiscal year. However like much of the industry, costs and the price of oil have taken a toll.

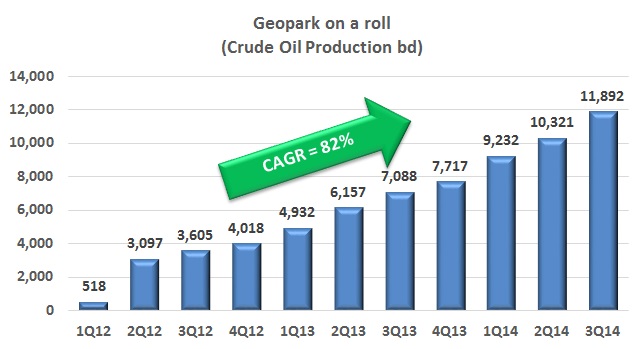

Latin American oil and gas producer Geopark (NYSE:GPRK) saw its overall production grow 66% year-over-year to reach 21,548bd in its overall production, with a 68% increase in Colombia to reach 11,934bd.

Ecopetrol (NYSE:EC) has inaugurated a new water treatment facilities in Acacías, Meta, which the NOC says will allow it to quickly increase production in the Castilla field by an additional 30,000bd.

Perenco said last week that it would shut down its operations in Aguazul after three months of blockades from the Tesoro Bubuy village. The action apparently was enough to bring the community to the table and lift the blockades, although talks still remain.

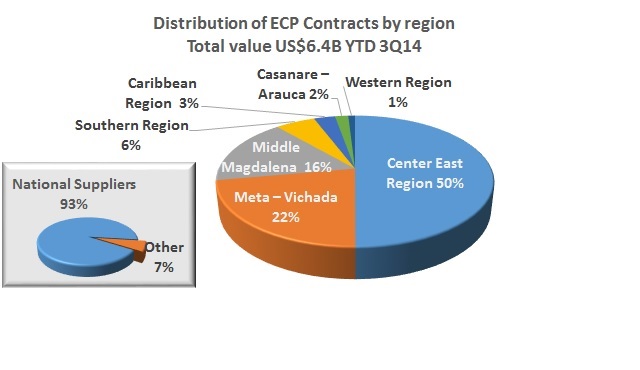

Ecopetrol (NYSE:EC) says that it has spent CoP$13.27T (US$6.27B) on goods and services during the first nine months of 2014, with 93% of that total going to suppliers based in Colombia.

Ecopetrol (NYSE:EC) had set a production target of 819,000boed for 2014, but with its average after three quarters sitting at 754,800boed, the NOC will almost certainly fall short of its goal.

Parex Resources (TSX:PXT) posted production and financial gains, growing production 27% sequentially, while revenues increased 24.9%.

Gran Tierra Energy (TSX:GTE) reported its third quarter earnings for 2014, and said that production and revenues had increased back above a dip experienced in the previous quarter. But considering its trend line over the last 7 quarters, its performance remains relatively flat, with oil prices and logistical issues on the OTA pipeline a recurring problem.

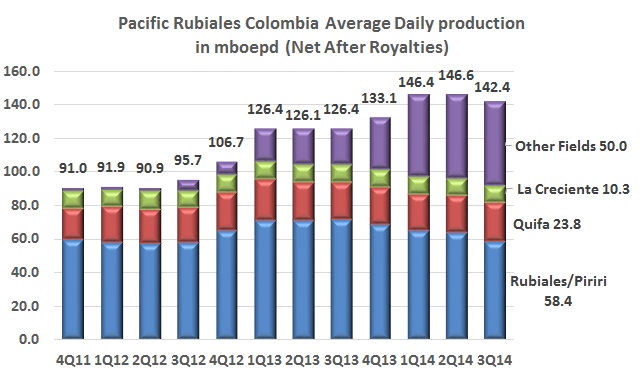

Production for Colombia’s largest private oil operator Pacific Rubiales (TSX:PRE) dropped in the third quarter of 2014 compared to the previous quarter, as water disposal issues continue to affect its flagship Rubiales field. Management looked to focus on the opportunities for other fields and expectations for Mexico, while ensuring that it would stay in Rubiales and that production would grow.

2026, Hydrocarbons Colombia, All Rights Reserved.