The director of the National Planning Department (DNP) and Ecopetrol (NYSE:EC) board member Simon Gaviria says that the NOC is preparing a dividend proposal that looks to protect its investment grade rating, and avoid being classified as a junk.

Alarms from environmental groups in Casanare has put a seismic campaign planned by Canacol Energy (TSX:CNE) into a firestorm of controversy over a permit to extract water from the Cravo Sur River.

The controversy surrounding the soaring costs to modernize the Cartagena Refinery (Reficar) has hit new heights (or are they lows?), with control bodies promising to investigate former management, presidents accusing presidents and much more.

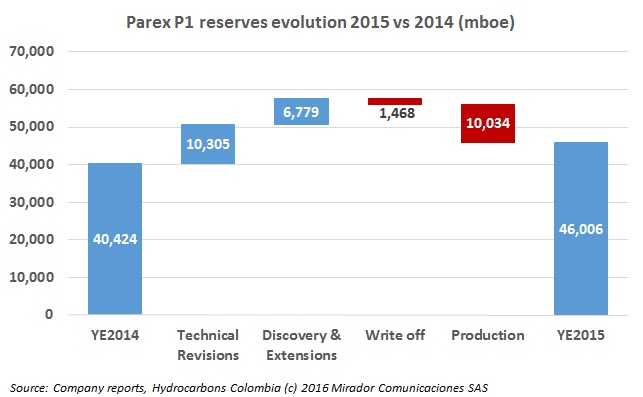

Parex Resources (TSX:PXT) reported its 2P reserve assessment for 2015, and said that it grew its proved plus probable reserves by 19% year-over-year, to log net 2P reserves of 81.7Mmboe as of December 31, 2015.

Pacific E&P’s management said in a recent interview that it is in strategic talks to find a long term solution to its debt payments, and that its robust operational portfolio could facilitate this discussion, but did not give more specifics.

Gas Natural Fenosa country manager for Colombia, Alberto González, said that the supply of natural gas is solid and that the firm will look to growth by introducing more gas-powered appliances in homes, and invest in infrastructure.

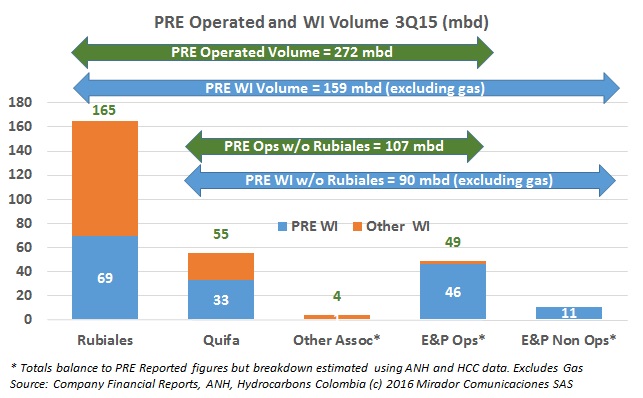

There is no avoiding the discussion: these days we cannot talk to anyone either in or outside of the industry without someone asking “What will happen to Pacific?” We cannot answer that nor we will we speculate. But we can provide some facts and estimates that we think illuminate the risks to total Colombian production in a ‘doomsday scenario’.

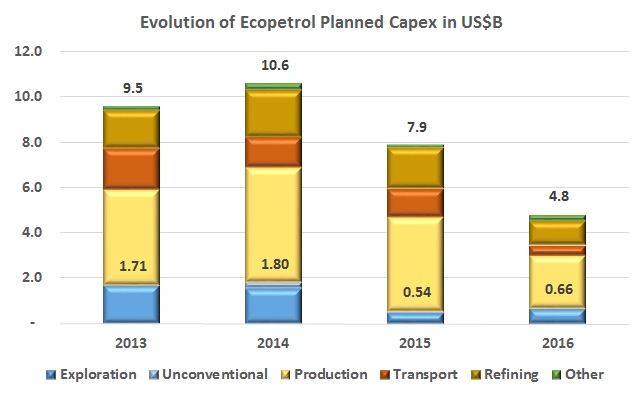

The Colombian Chamber of Oil Goods and Services (Campetrol) published an analysis of how Ecopetrol’s (NYSE:EC) exploration budget has shifted to market conditions over the last several years, and urged the NOC to step up exploratory efforts and spending.

The blame game is in full effect, and now the General Controller has said the Cartagena Refinery contractor charged with the cost laden modernization project CB&I (NYSE:CBI) is looking to pull out of Colombia without passing over documents requested by the control entity in an audit of the project.

Gran Tierra Energy (TSX:GTE) CEO Gary Guidry reaffirmed the operator’s focus on Colombia, and said that with low prices many projects will no longer be viable, presenting an opportunity for firms with a low cost structure. He also emphasized the importance of oil infrastructure.

2026, Hydrocarbons Colombia, All Rights Reserved.