The controversy surrounding overruns in the modernization of the Cartagena Refinery (Reficar) is not the only issue facing Ecopetrol (NYSE:EC) with potential to cause a public stir. The sale of petrochemical firm Propilco, despite Reficar synergies, and another problematic refinery project at Bioenergy are also present.

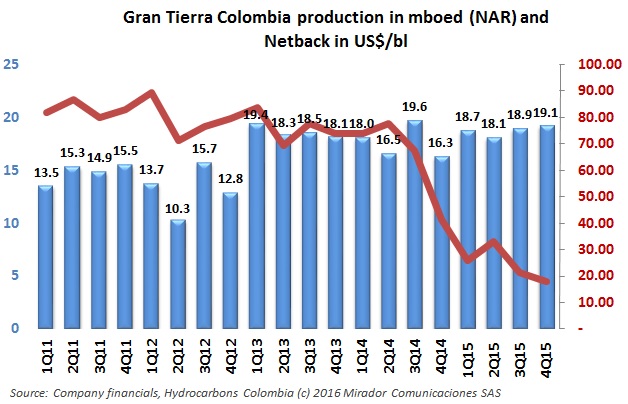

Gran Tierra Energy (TSX:GTE) says 2015 was a “transformational” year and it is in good financial shape to be competitive going forward. It posted a loss for the year of US$268M, but shrunk its loss in the fourth quarter by over 70% compared to the previous year.

A 2015 perceptions survey carried out by the Chamber of Oil Goods and Services (Campetrol) showed that almost no service companies could call 2015 a good year, and the association called for immediate action from the government to restart Ecopetrol’s (NYSE:EC) exploration program.

Pacific E&P (TSX:PRE) was the affected operator in another Constitutional Court decision regarding the prior consultation process and an indigenous group in Puerto Gaitán, Meta, which affects the operator’s operations in Quifa.

The National Hydrocarbons Agency (ANH) stepped up its position and said that it will sanction Santa María Petroleum, one of several firms accused of delivering false letters of credit to cover contract guarantees for an E&P contract.

The controversy surrounding the Cartagena Refinery (Reficar) has caused a moment of rare consensus across the political spectrum in Colombia’s congress: From the opposition bank of Senator Alvaro Uribe to the left leaning Polo Democratico and those between, all want to see a special session to grill those involved in the project.

Oil companies in Colombia and beyond are starting to see a “significant” loss of labor talent, says a recently published study on the oil and gas labor market from global recruiter Hays.

We came across two profiles of recent executive appointments in Colombia which warranted a bit more attention: the arrival of Andrés Acosta as the new president of ExxonMobil (NYSE:XOM) Colombia, and of Felipe Bayón Pardo as Ecopetrol’s (NYSE:EC) COO.

Ecopetrol (NYSE:EC), Equion, and Parex Resources (TSX:PXT) have all been activie in the Llanos, as the new Governor promises to create a space to facilitate dialogue and reduce social conflict. These and other Corporate Social Responsibility (CSR) stories in our periodic roundup.

Ecopetrol (NYSE:EC) says that the fall in oil prices has forced it to suspend wells temporarily in the Caño Sur field, in Puerto Gaitán, Meta. A local operations manager said it has already filed the request with the National Hydrocarbons Agency (ANH).

2026, Hydrocarbons Colombia, All Rights Reserved.