The Colombian State Council found that the firm Gran Tierra Energy Colombia (TSX: GTE) has failed to meet the terms of a contract with Ecopetrol (NYSE:EC) and therefore owes the state oil firm CoP$6.2B (US$2M).

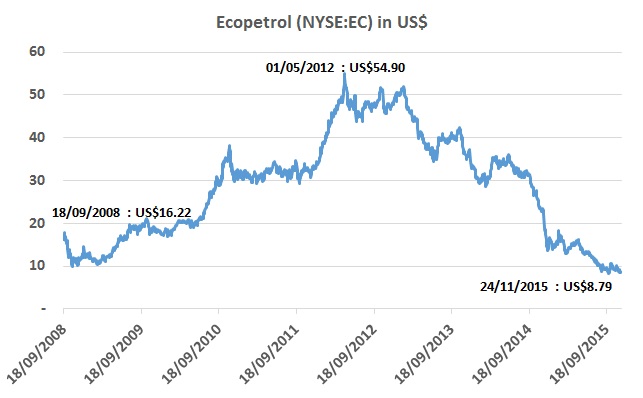

Thousands of Colombians invested their savings in Ecopetrol (NYSE:EC) following its market debut in 2007. Those that did not sell off at its peak have been left to watch their investment’s value shrink, and in early November the NOC’s stock fell below its IPO value on the Bogotá exchange. What options do these small investors have to recovery their lost value?

Ecopetrol (NYSE:EC) says it has finished a demonstration plant in Chichimene in the Meta Department which uses a technology to lighten heavy and extra heavy crudes, allowing them to be shipped in pipelines while cutting the company’s need to purchase naphtha as a diluent.

Improvised, illegal and dangerous valves installed along Ecopetrol (NYSE:EC) pipelines are causing it to lose a growing amount of crude, also resulting in risks of severe environmental damage.

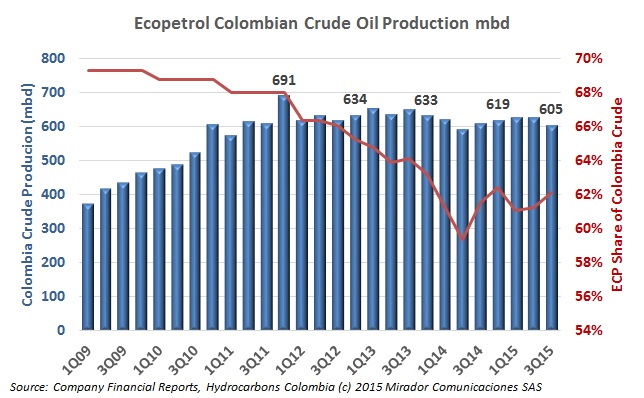

Ecopetrol (NYSE:EC) can celebrate that unlike nearly all of its private industry peers it has been able to post a profit in the third quarter of 2015, but it has seen its production fall slightly, and its E&P business continues to post losses. This has been compensated by its refining business to some degree, while transportation income nearly doubled.

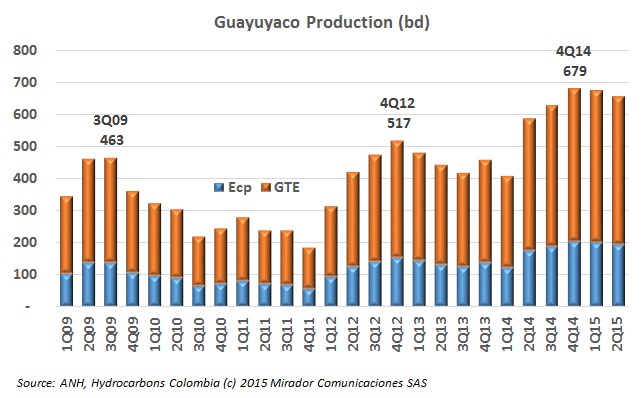

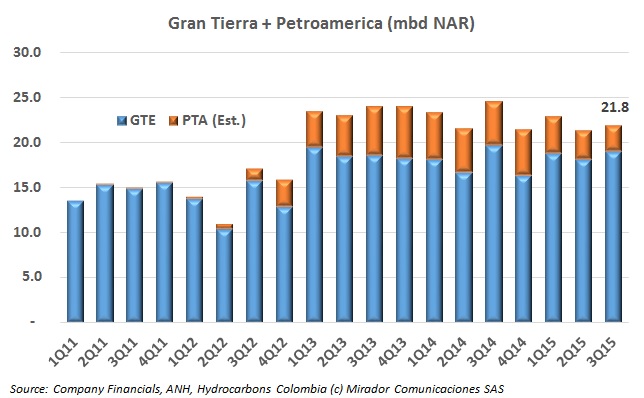

Gran Tierra Energy (TSX:GTE) says that it has entered into an agreement to acquire Petroamerica (TSX Venture:PTA), its first major move since new management took charge earlier this year, and a bid to consolidate its operation in Putumayo.

The USO is planning a general strike in Ecopetrol’s (NYSE:EC) fields and facilities on November 17th, which it claims is necessary to protect against mass layoffs being planned by multinationals.

In announcing Geopark (NYSE:GPRK) 3Q15 results, CEO James F Park said that the company’s portfolio and cost-management efforts resulted in “approximately 85% of our production being profitable at a $25-30 oil Price”.

The controversy surrounding the operation of Colombia’s largest producing field, Rubiales, continues past Ecopetrol’s (NYSE:EC) decision to operate the field on its own. Now statements from the Minister of Labor Luis Eduardo Garzón have ignited a debate on current operator Pacific E&P (TSX:PRE) workers at the field.

Canacol Energy (TSX:CNE) reported its third quarter 2015 results, which showed a sequential increase in production and a fall in costs, but gas production fell sequentially although up year-over-year.

2026, Hydrocarbons Colombia, All Rights Reserved.