The National Hydrocarbons Agency (ANH) announced the list of companies that will participate in the third cycle of the Permanent Competitive Process (PPAA). Here are the details.

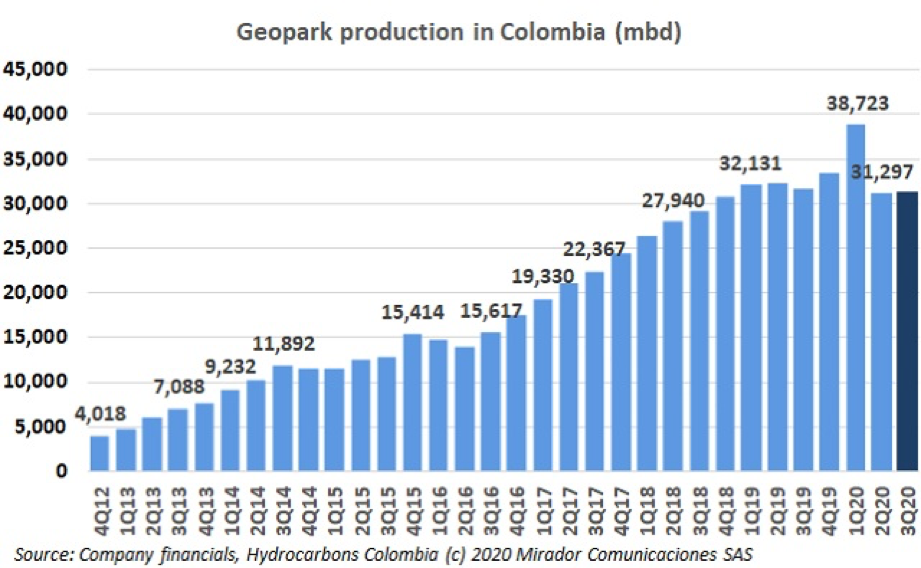

Geopark Limited (NYSE: GPRK) announced its operational update for the three-month period ended September 30th, 2020.

Ecopetrol (NYSE:EC) has managed to promote the growth of local entrepreneurs through its ‘Somos Colombia’ (literally: ‘We are Colombia’) virtual rounds. Here are the details.

The National Hydrocarbons Agency (ANH) announced the selection process for companies to develop fracking pilot projects (PPII) in Colombia.

Grupo Energía Bogotá (GEB) announced that the Board of Directors of Transportadora de Gas Internacional S.A ESP (TGI) appointed Mónica Contreras as the company’s new president.

The most recent report of the International Initiative for Transparency (EITI) explained the importance of the mining- energy industry for the national finances.

La Republica business paper conducted an analysis of the most profitable oil companies in Latin America. Ecopetrol (NYSE: EC) occupied a prominent position.

The government will start the socialization phase of fracking pilot projects (PPII) with communities in the Middle Magdalena Valley during November this year. Here are the details.

Frontera Energy (TSE: FEC) was recognized by the United Nations for its transparency policies.

2026, Hydrocarbons Colombia, All Rights Reserved.