Tuesday, July 14th, 2026

Colombia’s oil and gas production data for May 2026, compiled by Acipet from ANH figures and reported by Valora Analitik on July 9, confirms that the sector’s decline is accelerating – and that the gas side of the ledger is deteriorating far faster than oil.

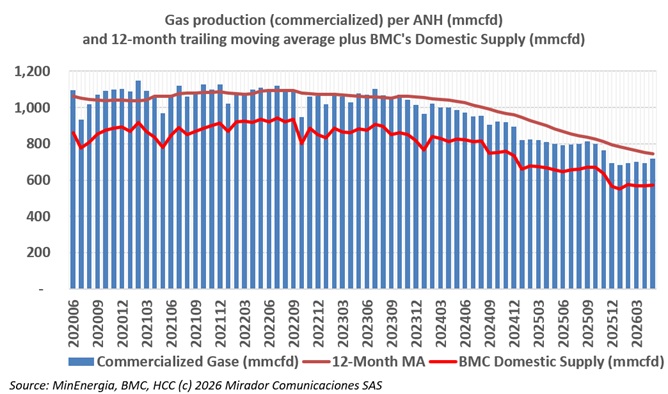

Tomás de la Calle is back, this time looking at the country’s declining gas reserves and wondering about the UPME’s role in getting us to here … and getting us back to self-sufficiency.

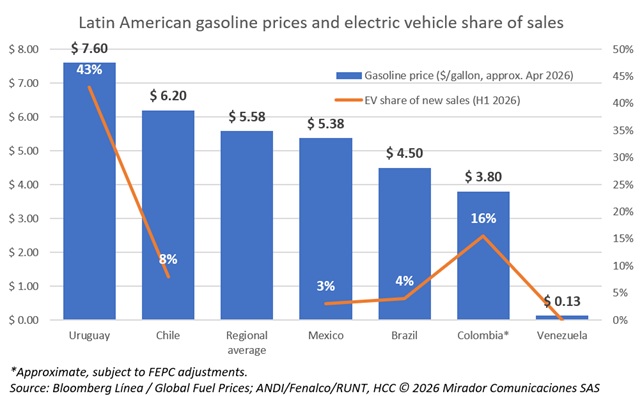

The conventional explanation for Latin America’s electric vehicle boom, as Bloomberg Línea documented for Uruguay this month, is straightforward: when gasoline costs US$7.60 a gallon – the highest in the region – the economics of switching to electric become irresistible.

The Alberta court’s June 24th authorization for Canacol to void its gas contracts has generated a widening circle of sector responses that go beyond the immediate Cerro Matoso crisis, touching distribution companies, the coal sector, industrial associations, and legal scholars, all of whom converged on a single point: the decisive chapter will be written not in Calgary but in Bogotá.

Two concurrent market developments are repositioning liquefied petroleum gas (LPG) as a strategic energy alternative in Colombia and both are being driven by the same underlying force: the accelerating collapse of domestic natural gas supply at a moment when imported gas is becoming too expensive for the country’s interior regions to absorb.

President-elect Abelardo de la Espriella has confirmed ten of his ministers with just under a month until his August 7th inauguration, in a process that Cambio Colombia tracked across multiple rounds of announcements.

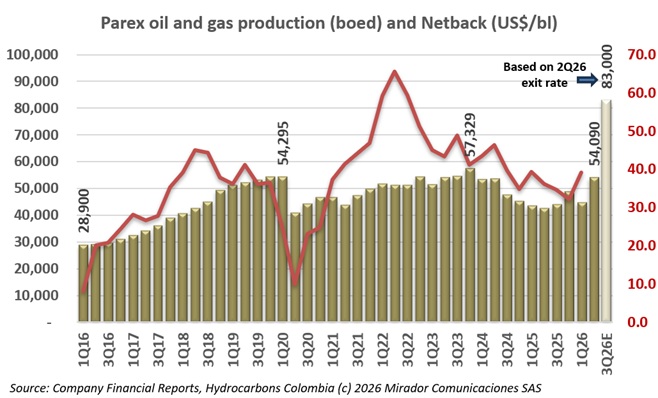

Parex Resources reported a 2Q26 average production of 54,090 boed on July 6th, a figure that understates the company’s transformed scale because it blends two months of pre-acquisition operations with a June that was fundamentally different.

2026, Hydrocarbons Colombia, All Rights Reserved.