Petrobras and Ecopetrol confirmed a new natural gas discovery with the drilling of the Sandía-1 exploration well, located in the GUA-OFF-0 block in deep water offshore Colombia.

GeoPark completed a strategic reset in 2025, exiting Ecuador and Brazil to concentrate on two markets: Colombia as its cash-generating base and Argentina’s Vaca Muerta as its new growth engine in unconventional resources.

Deutsche Bank’s assessment of a fast-developing El Niño episode – potentially among the six most intense since 1870 – named Colombia as Latin America’s most exposed economy, projecting the country’s price index could rise roughly 1.4 percentage points before year-end, the largest inflationary impact in the region alongside Peru’s 1.1 points.

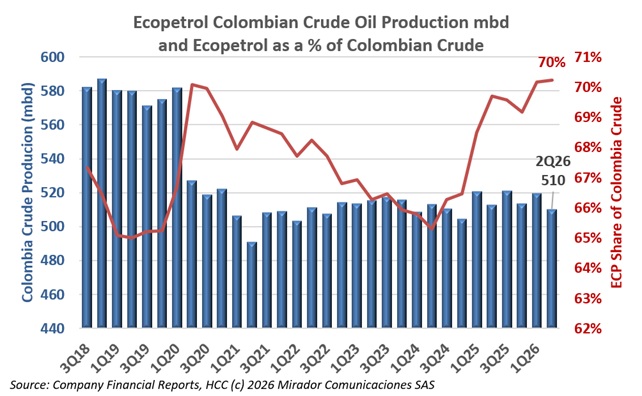

Grupo Ecopetrol reported second-quarter 2026 results reflecting what the company described as its ability to maximize an integrated strategy and respond with agility to market dynamics.

President Gustavo Petro signed Decreto 0905 on July 30th, naming Edwin Palma – currently Minister of Mines and Energy – as ad hoc Minister of Labor and ad hoc Minister of Housing, City, and Territory, concentrating three portfolios in one official just a week before the administration’s term ends on August 7th.

Decreto 0526 de 2026 has raised alarms in Cauca after the Compañía Energética de Occidente (CEO) warned the measure will alter the Fondo de Energía Social (FOES) and could push energy bills up by as much as 30% for roughly 178,000 users starting June 1, 2027.

2026, Hydrocarbons Colombia, All Rights Reserved.