Wednesday, June 10th, 2026

The Colombian stock market became briefly the best-performing bourse in the world on June 1, with the MSCI Colcap index surging around 6% in early trading after Abelardo de la Espriella topped the presidential first round with 43.7% of the vote, a margin well above what Wall Street consensus had expected.

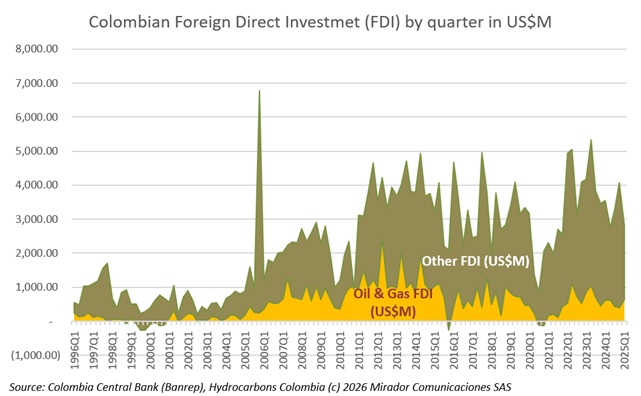

Foreign direct investment in Colombia’s oil sector fell more than 7% year-on-year in Q1 2026, reaching US$589M against US$634M in the same period of 2025, according to Banco de la República data.

If Abelardo De la Espriella wins the June 21 runoff, Colombia’s upstream sector should expect an immediate and deliberate reversal of the Petro administration’s anti-hydrocarbon posture.

Colombia’s liquefied petroleum gas (LPG aka propane) sector is heading into a structural supply gap, and a new Cartagena terminal is positioning itself as the primary solution

Vaca Muerta is already producing 597,300 bd from the Neuquén basin, representing two-thirds of Argentina’s national output of 885,300 bd — and Luis Barallat, BCG’s director for Iberia and South America, believes that is still early innings.

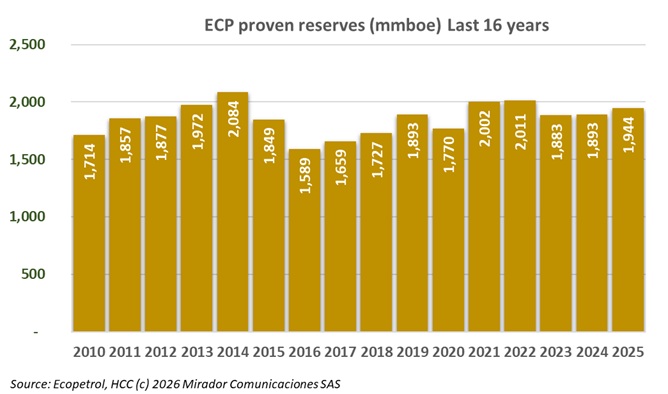

Ecopetrol closed 2025 with a reserve replacement index of 1.21 – meaning it added 1.21 equivalent barrels to its proven reserves for every equivalent barrel it produced during the year. Against annual production of 248 million equivalent barrels, the company incorporated 300 million equivalent barrels of new proven reserves, a result the Asociación Colombiana de Ingenieros de Petróleos (Acipet) characterized as positive for the state oil company.

A year ago, Ecopetrol and Transportadora de Gas Internacional (TGI), the pipeline subsidiary of Grupo Energía Bogotá, were competing fiercely to build Colombia’s next LNG import terminal on the Caribbean coast, each claiming its project was the faster and more technically viable path to first gas in early 2027. Both promises have since deflated.

2026, Hydrocarbons Colombia, All Rights Reserved.